Mortgages for First-Time Buyers in Northern Ireland.

Helping you buy your first home sooner — even with a small deposit.

Friendly, straight-talking advice from a local Belfast mortgage broker who has helped 500+ first-time buyers get on the property ladder.

⭐ 5 Star Google Reviews

🏡 500+ First Time Buyers Helped

📍 Belfast Based Specialists

Mortgages for First-Time Buyers in Northern Ireland.

Helping you buy your first home sooner — even with a small deposit.

Friendly, straight-talking advice from a local Belfast mortgage broker who has helped 500+ first-time buyers get on the property ladder.

⭐ 5 Star Google Reviews

🏡 500+ First Time Buyers Helped

📍 Belfast Based Specialists

Ways First-Time Buyers Buy Their First Home

Most first-time buyers think they need a huge deposit.

But there are several ways people buy their first home.

Low Deposit Mortgages

If you've managed to save 5% to 10% of the purchase price, you may already have enough to buy your first home.

Many lenders offer mortgages specifically for first-time buyers with smaller deposits.

For example:

£200,000 property

5% deposit = £10,000

The deposit doesn't have to be perfect either — many buyers use a mix of savings and gifted deposits from family.

The key thing is understanding:

• how much you can borrow

• what deposit you need

• what the monthly payments would look like

Low Deposit Mortgages

If you've managed to save 5% to 10% of the purchase price, you may already have enough to buy your first home.

Many lenders offer mortgages specifically for first-time buyers with smaller deposits.

For example:

£200,000 property

5% deposit = £10,000

The deposit doesn't have to be perfect either — many buyers use a mix of savings and gifted deposits from family.

The key thing is understanding:

• how much you can borrow

• what deposit you need

• what the monthly payments would look like

Buying Without a Deposit

Some first-time buyers manage to buy without saving a traditional deposit.

This is usually done in one of three ways:

Family Backed Mortgages

Some lenders allow family members to help by:

• gifting money

• using savings as security

• acting as guarantors

Buying Below Market Value

If you're buying from family members, sometimes the property can be sold to you below its market value.

The difference between the value and purchase price can count as your deposit.

Co-ownership

Several local lenders will use the share that Co-ownership buy as the full deposit with the client poutting down no money of their own.

These options aren't suitable for everyone — but when they work, they can allow buyers to get on the property ladder years earlier than they expected.

Co-Ownership Scheme

Co-Ownership is a scheme designed to help first-time buyers who can't afford to buy a home outright.

Instead of buying 100% of the property, you buy a share of it — usually between 50% and 90%.

You then pay:

• a mortgage on your share

• rent on the remaining share

Over time you can buy more shares until you own the property fully.

For many buyers, Co-Ownership reduces:

• the deposit required

• the mortgage needed

• the income required to qualify

Your Home May Be Repossessed If You Do Not Keep Up Your Mortgage Repayments.

Meet The Founder

Paddy Rice

When I went for my very first mortgage appointment, long before I ever became an advisor, I nearly walked away from the dream of owning a home.

The advisor we met looked down his nose at me and my (then) girlfriend. We were young, unsure of ourselves, and trying to figure it all out. He almost laughed us out of the office. We left feeling embarrassed, judged, and convinced we weren’t “ready.” It put us off buying for a long time.

Years later, when I became a mortgage advisor myself, I realised something that changed everything — we actually could have got a mortgage back then. We didn’t need judgment. We needed guidance. We needed someone to take the time, understand our situation, and show us the path.

That’s why I promised I would never treat people that way.

I launched First Time Buyer Mortgages for one simple reason: first-time buyers need the most help. You’ve never done this before. You might feel unsure. You might even have had a bad experience elsewhere. That’s exactly why we exist.

We take the time to get to know you, your plans, and what matters most to you. With access to a wide panel of lenders and years of experience helping over 500 people secure their first home, we guide you step-by-step through the process and recommend a mortgage that genuinely fits your life.

No pressure. No judgment. Nothing is too much trouble.

Just honest advice and real support — so you can finally get the keys to your first home.

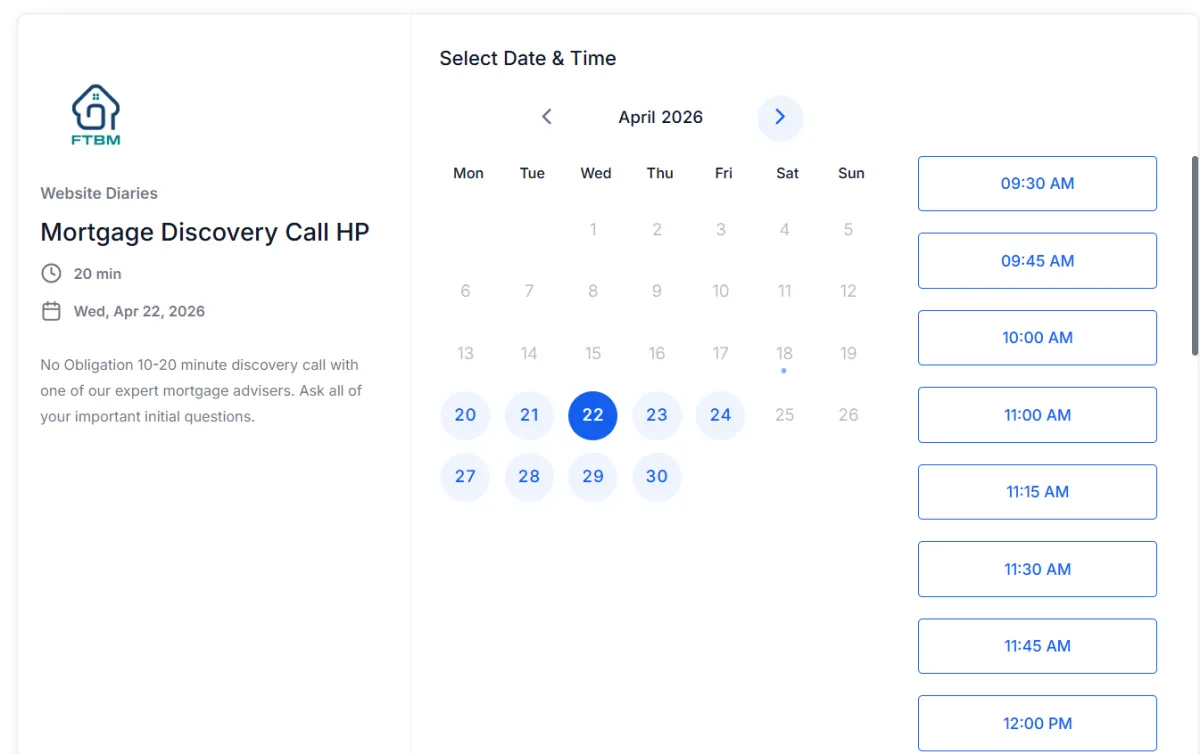

Book Your Initial 15 Minute Mortgage Qualification Call

On the call;

We will answer your most important questions

Complete a quick affordability check

Assess if there is any urgent action you need to take

Recommend your best next step

Highlight key resources to get prepared for your first home

15 minute telephone call - totally FREE

Meet The Founder

Paddy Rice

When I went for my very first mortgage appointment, long before I ever became an advisor, I nearly walked away from the dream of owning a home.

The advisor we met looked down his nose at me and my (then) girlfriend. We were young, unsure of ourselves, and trying to figure it all out. He almost laughed us out of the office. We left feeling embarrassed, judged, and convinced we weren’t “ready.” It put us off buying for a long time.

Years later, when I became a mortgage advisor myself, I realised something that changed everything — we actually could have got a mortgage back then. We didn’t need judgment. We needed guidance. We needed someone to take the time, understand our situation, and show us the path.

That’s why I promised I would never treat people that way.

I launched First Time Buyer Mortgages for one simple reason: first-time buyers need the most help. You’ve never done this before. You might feel unsure. You might even have had a bad experience elsewhere. That’s exactly why we exist.

We take the time to get to know you, your plans, and what matters most to you. With access to a wide panel of lenders and years of experience helping over 500 people secure their first home, we guide you step-by-step through the process and recommend a mortgage that genuinely fits your life.

No pressure. No judgment. Nothing is too much trouble.

Just honest advice and real support — so you can finally get the keys to your first home.